Achieving absolute return targets in multi-asset funds is very different and, in my opinion, much more difficult to achieve than relative return targets and requires a completely different approach.

Any honest fund manager will be the first to confess that they do not have a crystal ball but still somehow has to produce consistent positive results through a combination of assets where the individual return expectations are not clear. This is an additional requirement for absolute return mandates, as out-performance (or at very least matching) of benchmarks within asset classes remains as critical as in relative benchmark portfolios. The fact is that any specific return above the risk free rate cannot be guaranteed for any specific time period, and that is assuming the concept of risk free rate even exists. That is where risk management becomes vital, as it provides the ability to achieve targets with relative certainty and confidence over rolling periods by not only targeting specific risk levels of risk as opposed to return, but doing so in the most optimal way, thus mitigating the volatility and producing a smoothed return of the optimal level of risk through diversification.

The process of optimisation that is used by such fund houses as MitonOptimal is based on Markowitz portfolio theory and requires three inputs: a measure of return, a measure of risk and a measure of correlation. They use volatility as measured by standard deviation of returns as a measure for risk, and variances and co-variances between all pairs of asset classes for correlations, making the approach a form of Mean Variance Optimisation.

Even though the theory behind this is well known and could (and quite frankly should) be used and even replicated by everyone, MitonOptimal does employ a few proprietary alterations to the traditional model, which tailor make it to fit their own needs and beliefs. This includes exponential time weighting of risk and correlation measures to adapt to changing market conditions, as well as not purely using historical returns given their belief that asset class returns are cyclical, among other things.

All adjustments are based on rigorous testing and re-testing in order to make it as robust and yet sophisticated as possible to give sensible results in all possible market conditions. It is also essential for any model to be adaptive to a change in the tides, and steer portfolios in the right direction even if there is an unexpected game-changing event, as that is exactly when investors find the benefit of protection through diversification most valuable.

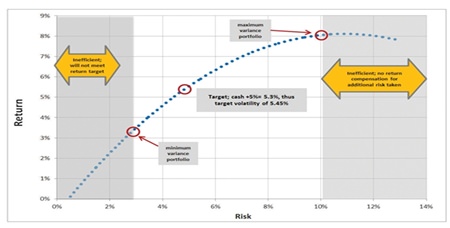

The optimisation process is thus aimed at producing a target level for risk that corresponds to the targeted return at the point where it has the highest Sharpe ratio, given the model inputs. This would be the “neutral” portfolio which sets the guidelines for a long term strategic investment plan to achieve the absolute return target.

Optimising for a static portfolio at this point is not good enough though, the Strategic plan needs to accommodate for Tactical deviations as markets move through short/medium term cycles creating trading opportunities. Multiple combinations of asset classes are tested and optimised and (given the parameters) together form an efficient frontier of all possible optima; risk adjusted return levels (highest return at any given risk, or lowest risk at any given return). Calculating an upper and lower target on the efficient frontier given minimum return targets and effective risk allocation thus produces a minimum and maximum variance portfolio.

By this point the fund manager should have minimum and maximum allowances by asset class as a result of all the different permutations tested, as well as a neutral for each asset class as per the neutral portfolio, dictating some parameters.

If the minimum variance portfolio is viewed as the 0/10 portfolio, the neutral portfolio is 5/10 and the maximum variance portfolio 10/10, any given combination of assets can be risk rated on a scale of 0-10. The figure 5 thus represents the Strategic plan, and the average risk rating over long periods of time should essentially be close to that. But tactical moves closer to 0 (in ‘risk off’ periods) or 10 (in ‘risk on’ periods) offer major return enhancing opportunities based on shorter term market conditions and pricing anomalies moving asset classes away from their perceived intrinsic values. Return attribution, in decreasing order of importance, is driven by:

1. The Strategic plan

2. Tactical moves up and down the risk spectrum (0-10)

3. Tactically over and under-weighting specific asset classes

4. Tactically over and under-weighting sectors within an asset class

5. The manager/security selection

The optimisation process by no means replaces a fund manager; it is purely an additional tool for understanding, controlling and measuring risk as well as providing guidance and controls towards confidently achieving absolute return targets. An added benefit of the process is that it is possible to attribute returns for any given period to any of the five points mentioned above. This gives the fund managers the tools to assess where there is added/detracted value and improve on necessary areas whilst leveraging off skills where they are adding value. Thus this is an ongoing process which never stops and is constantly evolving and is why Absolute Returns Funds should be part of your portfolio – absolutely!

{kind=link}