The Grant Thornton International Business Report (IBR) for H2 2023, which measures sentiment amongst mid-market business leaders, shows a considerable drop in overall business health across Thailand. Intensifying pressure from neighboring economies, combined with growing pessimism for the private sector, are largely driving this steep decline in economic outlook. Grant Thornton’s biannual report consolidates surveys and interviews from mid-market businesses, analyzing market sentiment through anticipated trends and business conditions for the upcoming 12-month period.

The H2 2023 IBR findings are striking, in that they reveal a significant departure from the otherwise consistent trend of positive sentiment among business leaders in recent economic periods. Expectations of strong post-pandemic growth have given way to resignation, at least for now — a revealing and sobering reflection of numerous issues simmering within the Thai economy. These challenges include a constrained export market, declining productivity, and an ageing and shrinking workforce that is proving inadequate to the demands of a progressively digital economy.

Stormy horizons

At a global level, scores on mid-market business health rose once again to 3.8 on the index score during the current period, a positive indication for the worldwide economy as this number had been in negative territory just twelve months prior.

Reassuring as these global figures may be, the data shows trouble brewing at a regional level. Asia-Pacific and ASEAN both reported a dip across outlook and restriction indicators, as well as their overall totals. Asia-Pacific’s current business health score is now at 0.4, with ASEAN down by 2 to 7.9.

Thailand’s business health score represents an even more notable dip, falling 5 points from the previous period to 9.3. This total reflects a worsened climate for investment, weaker economic conditions, and a particularly sharp decrease in overall business optimism.

Despite this gloomy image, the expected restrictions for mid-market businesses in Thailand remain relatively unchanged. Supply constraints and economic uncertainty, for example, are perceived as less significant obstacles now than they were six months previously, improving by 1 and 3 points respectively. The easing of political tensions likely also contributed to an improved perception during this period. It was economic outlook, which decreased drastically by 10 points, that drove the decline in Thailand’s business health metric.

Growing pains

A deeper look at the survey responses from Thai businesses tells an interesting story. Fueling the negative trajectory of business health, the percentage of businesses expecting an improvement in economic optimism over the upcoming 12-month period has fluctuated immensely in recent campaigns — from 54% in H2 2022, then surging to 72% in H1 2023, and receding again to 55% in H2 2023. This decline positions the country’s optimism scores below both the regional and global averages, despite rising above all averages only six months prior.

The waning optimism is likely linked to reports of the actual annual GDP figures, which is expected to fall below the Finance Ministry’s forecast of 2.8%, primarily due to contractions in the manufacturing and export sectors. GDP growth only grew an estimated 1.8% in 2023. Additional factors for the private sector in Thailand, including substantial debt repayment levels and a debt-to-GDP ratio growing at a rate of 8.44% annually are further contributing to the diminishing optimism.

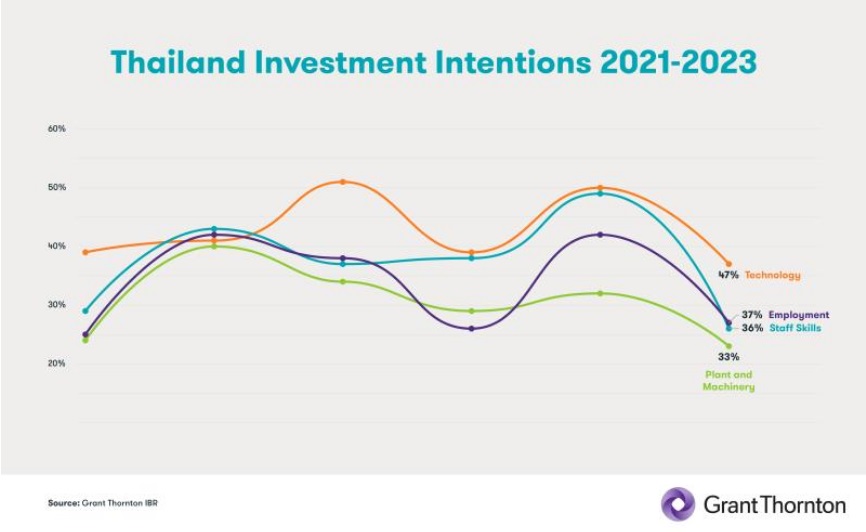

During the same period, Thailand’s revenue scores are down (from 73% in H1 2023 to 58% now), profitability expectations are lower (from 82% to 79%), and exports likewise follow a similar trend (from 46% to 42%). In terms of future investment intentions, employment scores are also down (from 52% to 37%); as are those for investment in staff skills (59% then, 36% now), and investment in technology (from 60% to 47%). Neighboring countries persistently and increasingly produce impressive numbers on these metrics, lifting ASEAN averages higher than Thailand’s scores here.

An explanation for this disparity can be found in the lack of innovation present in Thailand compared to its regional counterparts – a concerning development that should prompt the Thai government to invest more in education, enhancing workers’ skills, and breeding a strong competitive landscape in ways that stem beyond short-term stimulus type measures.

Survey responses suggest that many in the business community share the same view on the efficacy of current government stimulus measures. Respondents were queried about their outlook on the government’s THB 10,000 handout initiative for individuals over 16, designed to stimulate the economy. Among the 104 respondents, 27 expressed a ‘very pessimistic’ view, while just 17 were ‘very optimistic.’ The remaining responses — more than half of the total — indicated a neutral stance, showing limited confidence in the fiscal stimulus measures intended to be deployed by the Thai government in 2024.

Amidst the constraint indicators, where lower scores indicate better performance, economic uncertainty remained relatively low in Thailand compared to regional and global averages, scoring 47% overall (slightly better than in the previous period). Other loosening constraints on mid-market business growth in Thailand include regulation & red tape (from 32% to 28%), finance shortage (21%), and energy costs (44% then, 39% now).

Despite remaining a lower concern for Thailand than global and regional averages, expectations of the availability of skilled workers (24% then, 26% now) worsened for the first time since H1 2021, indicating a rising awareness of the demographic shift toward an ageing society and its associated challenges. Additionally, these numbers highlight a growing dilemma whereby technological progress is outpacing the availability of skilled personnel proficient in utilizing the latest systems to enhance business performance and outcomes.

According to the survey responses, investment intentions of mid-market businesses are steering in the wrong direction. The evident decline in intent to invest in staff skills, technology, and plant & machinery, all plummeting by over 10 percentage points, paints a picture of the Thai economy akin to a dwindling flame losing its radiance. The bleak outlook is worsened by neighboring economies’ persistent growth, potentially pushing Thailand – a once vibrant and booming economy – into the background. Evidently, Thai businesses must prioritize strategic investments in innovation and workforce development, while the government reevaluates and enacts its fiscal stimulus policies, to ensure the economy’s resurgence and lasting prosperity.

The H2 2023 is based on approximately 4,900 surveys and interviews with global mid-market business leaders around the world, including 104 in Thailand. These interviews were conducted from October to November of 2023, and focus on the sentiment felt for the subsequent 12-month period rather than on current conditions. Scores for business health are determined by a weighted sum of positive and negative responses, ultimately falling within the range of -50 to +50. Results for business conditions and future investment intentions were scored by the percentage of businesses expecting an increase over the next 12 months. Results for business constraints were scored by the percentage answering 4 to 5 on a 1-5 scale where 5 is a major constraint. We would like to thank Oxford Economics for their assistance in analyzing and interpreting the results presented in this report. (NNT)

{kind=link}