At the Sunday, October 13 meeting of the Pattaya City Expats Club, well known Bangkok lawyer Mike Doyle’s topic was “Avoiding Legal Catastrophes in Thailand”. He spoke about some of the most common legal mistakes that foreigners make in Thailand and how to avoid them. Using real life stories, he focused on the areas of estate planning, employment law, and real estate acquisition.

Mike is a frequent public speaker in Thailand and the region on Thailand investment laws and is fluent in both written and spoken Thai. Mike is a US lawyer and Senior Partner of the Bangkok-based law firm Seri Manop & Doyle. He has practiced in Thailand since 1996 and in 1999 joined the firm and became a named partner in 2002. He first published his very well-known book Doyle’s Practical Guide to Thailand Business Law in 2004 (currently in its 5th edition – available in English and Japanese) and went on to publish Doyle’s Practical Guide to Business Law in Asia in 2009 (currently in its 2nd edition).

Mike introduced his talk on a light note, with a slide showing a Maclean’s magazine cover page with the stereotype of lawyers as rats. During his talk, he showed that often they deal with clients who try to cheat or are being cheated.

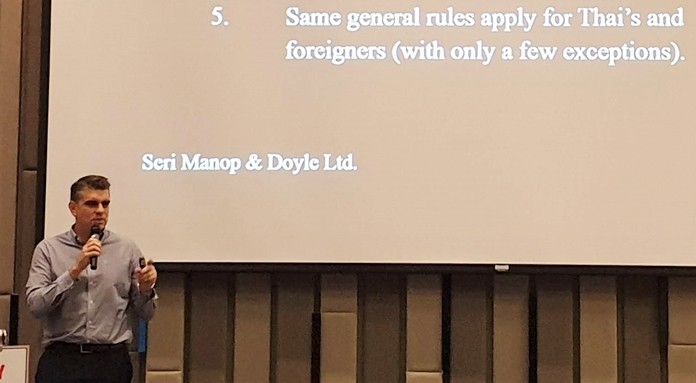

He began with the following observations on Thailand Estate Law: 1) If you die without a will, Thailand’s intestate rules apply on who will get your assets, 2) wills must be properly executed (normally not an issue), 3) foreign wills are generally enforceable in Thailand unless contrary to Thai Law, 4) Thai law does not recognize trusts, a common method in other countries to distribute assets over time to beneficiaries, and 5) the same general rules apply for Thais and foreigners with only a few exceptions.

Mike gave a case history of a Swedish entrepreneur with 2 wives and a son. The Swedish guy was married in his twenties to a Thai lady, marriage registered and had a son. He established a business which became very successful; 15 years later, they separated, but did not divorce. Five years after that, the man marries again, but does not register the marriage since he had not divorced his first wife. When he died, he did not have a will. Consequently, under Thai law, the first wife and sons inherited his assets and his second wife got nothing. The lesson to be learned from this is if you have assets in Thailand, you should have a will as it allows you to designate who is to receive your assets (including company shares).

The second aspect of Thai Law that he dealt with was when a company, a Japanese Jewelry manufacturer, wanted to remove their Financial Controller, caught stealing, and have their company property returned. The CEO in Japan decided to terminate him, but they discovered because they had also made him a Director, they must call a shareholders meeting which required a 7 day notice. Although no longer a company employee, during those 7 days, the director had the right to enter the company premises, thus still able to remove valuable property.

In the next situation, the company terminated the accounting manager in possession of the only company seal, a USA company with registered sales office in Thailand. There is a 45 million baht company bank account, but the accounting manager effectively controls access to the bank account because it requires use of the seal. The important lesson in this case is that there should be more than one company seal, otherwise the one person who possesses the seal will have the company at a disadvantage during negotiations for its return.

The next case study involved another situation involving a Financial Controller found to be embezzling funds. In this case, a Korean service company identified suspicious transactions to a supplier which turned out to be owned by the Controller and her husband. The decision was made to terminate the financial controller but was complicated by the fact that she was a company shareholder. The lesson here referred to how risky it can be to have staff serve as nominee shareholders because it gives them leverage.

In conclusion, the final case involved a situation many are familiar with, real estate purchase of buying a condominium off plan before construction. A French individual bought 5 condominium units off plan for 62 million baht, paying 80% up front to get a big discount. In this case, the land being developed was mortgaged to a bank. When the developer ran out of money and defaulted on the loan, the bank had first priority in their claim against the developer with buyers’ claims being secondary and they got nothing as there were no assets left to recover from. The important lesson is if you buy off plan, you are an unsecured creditor (just like a credit card company). Since buying off plan is a big risk, Mike recommended you do as much investigation as possible of the developer before investing anything, such as previous project bankruptcy. He emphasized it doesn’t matter what they say or what their offices look like as they are often very underfunded. The bank will lend money because it is secured by a mortgage. If it goes to court, the bank will be first in line and there will be many ahead of the lowly investor.

After the presentation, the MC brought everyone up to date on upcoming club and other Pattaya events of interest. The meeting ended with the usual Open Forum where audience members can ask questions or make comments about Expat life in Thailand, especially Pattaya. For more info about the PCEC, visit their website at http://pattayacityexpatsclub.com/. Visit the Club’s You Tube Channel at https://www.youtube.com/channel/UCJ2hH8irBpX_v7Qb7s-pANA to view the presentation and the subsequent speaker interview by Club member Ren Lexander.

|

|

|

{kind=link}