As an advocate of gold for most of the last 10 years but who has spent the last 18 months or so viewing the yellow alternate currency as asset to trade rather than hold, I’m asked frequently for my views on what has been typically represented as much as 25% of my own portfolio holdings throughout almost all of the 21st century, other than following ‘sell’ recommendations issued in November 2011.

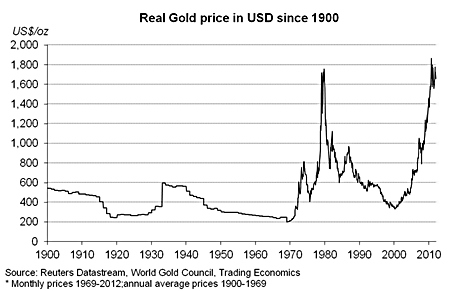

My colleague, Nic Craven, recently wrote that gold’s meteoric rise in price from the turn of the century has attracted a great deal of interest from investors, particularly as shares have been relative relatively flat in comparison. Much of the argument for investing in gold reflects it being seen as just another form of money, consistent with history going back to at least 700 B.C. As a store of value, more limited supply means that gold should be less affected by the gradual erosion of inflation – which has seen the US Dollar lose 98% of its real value since the early 20th century. Indeed, over the same timeframe, the price of gold in real (inflation-adjusted) terms has nearly tripled. The value of gold as an inflation hedge and a perceived safe-haven store of value make it attractive when confidence in paper money falls dramatically, as well as deflationary times such as during the great depression.

Over the long run this has led to a boom-bust cycle for gold, driven by the traditional business cycle. This means that gold needs to be treated with a balanced, somewhat contrarian view as an asset class like any other, with a cautious approach when prices are high and perceptions of risk are lowest. Opportunities are greatest when expectations for gold are low.

To date, our track record at managing this cycle has been extremely successful for investors. In 2000, at the onset of the current deflationary cycle, we recommended gold holdings for 10-25% of investor portfolios. At a price of around $270 per oz., gold had significant upside compared to risk assets such as equities and property, which looked relatively expensive. Since then we have recommended several periods of profit taking when prices had seemed to run ahead of themselves, which have limited clients’ exposure to gold price declines. Since the 2011 sell recommendation we have profited from range bound gold by selling when gold has approached $1800 per oz. (Comex) and buying at or below $1600. Over this 13 year period, the cumulative profit from these recommendations is a gain of +734% on original capital.

Value as protection against equity declines?

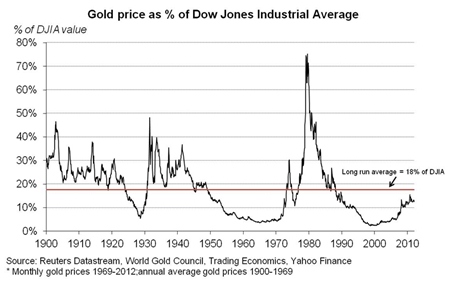

Gold’s performance vs equity markets can be another way to look at its value, although the logic of the link between the price of gold and a measure of the economy’s productive capacity is slightly more tenuous. Despite being close to historic peaks in real terms, gold’s current price is around 30% below its long-run average level against the Dow Jones Index. Given our concerns about equity market valuations, however, we’d be reluctant to interpret this too positively for gold, as it could equally be another indication that stocks are overvalued or at least a combination of gold under valuation and equity over pricing!

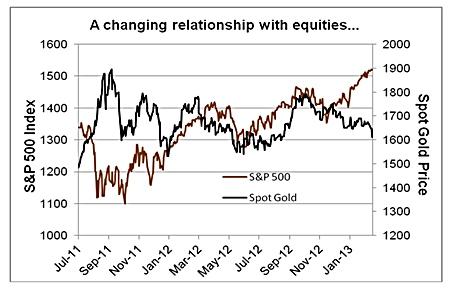

Arguably the more useful comparison of gold vs equities is the metal’s value as a “disaster hedge”, as it tends to attract investors when uncertainty about the real economy is greatest. Gold has historically risen in value during more extreme share market selloffs, giving useful diversification benefits alongside an investment in shares. However, the same doesn’t hold true for all periods of market weakness. In fact, since late 2011 gold has not delivered much in the way of protection from the gyrations of equity markets, tending to rise and fall in lockstep with equities. Only recently (since late 2012) has the correlation between gold and equities turned negative again – but not in gold’s favour, as this has largely been through gold prices tailing off while equity markets have rallied.

To be continued…

| The above data and research was compiled from sources believed to be reliable. However, neither MBMG International Ltd nor its officers can accept any liability for any errors or omissions in the above article nor bear any responsibility for any losses achieved as a result of any actions taken or not taken as a consequence of reading the above article. For more information please contact Graham Macdonald on [email protected] |

{kind=link}