The shenanigans in Washington over the last few weeks have been fascinating. Will they make a deal or not and at what cost to each party? It has been brinkmanship gone mad and all for the sake of face and one-upmanship.

There has been a non-ending flow of information on what would happen if America defaulted on its debt. These have ranged from all the major indices falling like lead balloons, worldwide recession, the Chinese making nasty threats which would cause even more havoc, US protectionism raising its ugly head again and a whole lot more. We now know a deal has been made but it is just kicking the can down the road. The reality of the situation is that there has to be a solution to the supposed USD17 trillion (yes, trillion!) the US is in hock to – it is actually a lot more if you take into account things like pensions, salaries for government employees, etc. No-one, not even the US, can go on pretending there is not a problem. The debt has to be repaid. It is just a matter of when and how.

One thing is for sure, there are going to be huge changes in the marketplaces. I have talked before about the ‘New Norm’ and we are due some restructuring of how things are at the present and what will transpire into unfamiliar territory.

For a start, many people reckon that equities could become a much better haven than bonds. Also, interest rates will start to rise sometime soon – let’s face it they cannot get any lower! The two things alone are going to have a huge affect on the world and its economy. And what happens in the US could well dictate how the rest of us get on.

With regards to interest rates, there was a short-term surge when people were panicking over whether or not an agreement would be reached and so fear set in about America not being able to meet its obligations. Obviously, this particular worry has been put back into Pandora’s Box but only for a while. There will come a time in the near future when rates will go up for the medium to long term.

The thing is how do things go from here? In an ideal world, it would be great if America could stop spending billions each and every month buying ‘assets’ and slowly start to increase rates over the next couple of years. Markets are presently concerned that the continuation of such low rates are the reason for ‘bubbles’. This is always going to be a problem when you have such a thing as QE year after year.

The problem with the above Utopian scenario is that the recent impasse has put a real spanner in the works and will probably mean it will cost 50 percentage points in 2013 growth forecasts. This is not exactly what President Obama needs at the moment as all of this creates worry and doubts in the market. Uncertainty is not the friend of anyone involved in finance or investing – interest rates can go up unexpectedly, just look at what has happened to bonds over the last couple of weeks. Also, Credit Default Swaps have been very much in fashion recently as people are hedging against any potential default.

There is so much Fed money sloshing around that interest rates will have to go up soon which means that the cost of debt will also increase. It is here that the vicious circle starts. If rates start to rise then the cost of everything else goes up too. This means any profit on investments will go down as higher interest costs eat in to any margins.

So what to do? What can you say? The value of most, if not all, assets will be lower than people expect and the sensible ones will want to just keep ahead of inflation by a couple of points. This will keep portfolio volatility down which could be very important in the near future. As I have stated above, it is not the worst idea in the world to use some of you hard earned money and put it into some decent well known international companies. There is every chance they will perform better than most countries. Let’s face it, a lot of companies have more money than some countries (and most have more than America!).

With politicians more concerned about grabbing the headlines and being jobsworths, the nation which they are meant to protect has no chance so it is best to look at something that does not involve political posturing. This is especially true as this is not over yet. There are three more dates to keep in mind. Stephen Lewis from Monument Securities describes it best when he said, “It is a truce, not a peace” as we are reminded that on 5th January, the American government will run out of funds. Also, the new debt ceiling will finish on 7th February. However, the country may have enough to keep it going for a few weeks but that is it, so March is going to be an important month.

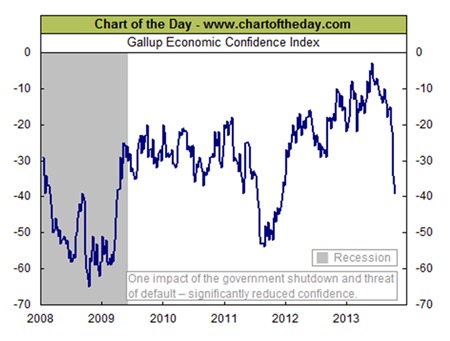

Consumer confidence is down to what it was five years ago as people realise America and, possibly, the rest of the world will be in limbo for five more months. Even World Bank chief Jim Yong Kim said the global economy had for now “dodged a potential catastrophe” but I wonder what he will be saying before Easter?

Unfortunately, the Americans have shot themselves in the foot. What the self-serving politicians have failed to realise is that the rest of the world has been appalled at the recent antics of the Tea Party et al. The Chinese are looking at reducing its one trillion dollars plus in US debt and putting into other asset classes. They are not alone and this will lead to a reduced demand for US Treasuries – not exactly a great advert for what is supposed to be the world’s leading economy. If the US does not come to its senses then the rest of the world will act by itself. As stated last week, there are opportunities out there – keep liquid and keep the faith.

As Will Rogers said, “Everything is changing. People are taking their comedians seriously and the politicians as a joke.”

| The above data and research was compiled from sources believed to be reliable. However, neither MBMG International Ltd nor its officers can accept any liability for any errors or omissions in the above article nor bear any responsibility for any losses achieved as a result of any actions taken or not taken as a consequence of reading the above article. For more information please contact Graham Macdonald on [email protected] |

{kind=link}